Home»Trade Essentials»Analysis of the Implementation Rules of the EU Government Subsidies Regulation

It elaborates in detail on the main provisions of the Implementing Rules of the EU Government Subsidies Regulation, especially the information disclosure requirements in merger and acquisition transactions and public procurement procedures. This includes basic information for merger and acquisition transaction filings, information on filing thresholds, information on foreign financial assistance, and information on assessing the impact of foreign financial assistance on the EU market. At the same time, the information disclosure requirements for public procurement procedures are also discussed with emphasis.

I. Scope of Information Provision in the Merger and Acquisition Transaction Filing Procedure

Basic information of merger and acquisition transactions: including an overview of the relevant merger and acquisition transactions, basic information of all parties to the transaction, and detailed information of the merger and acquisition transactions, especially the situation of obtaining control rights.

Information on filing thresholds: The Implementing Rules do not specifically refine the filing standards for turnover and total financial assistance. The total turnover and total financial assistance need to be calculated based on the entire group.

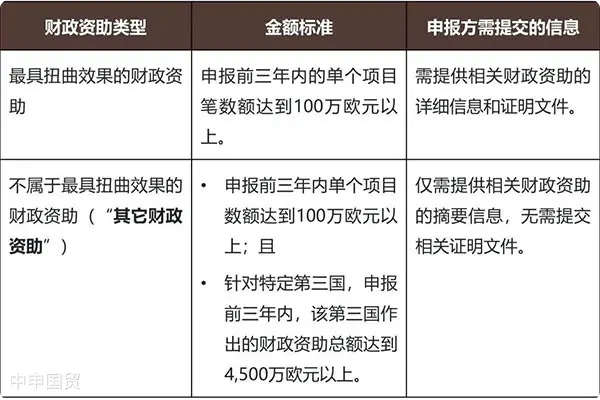

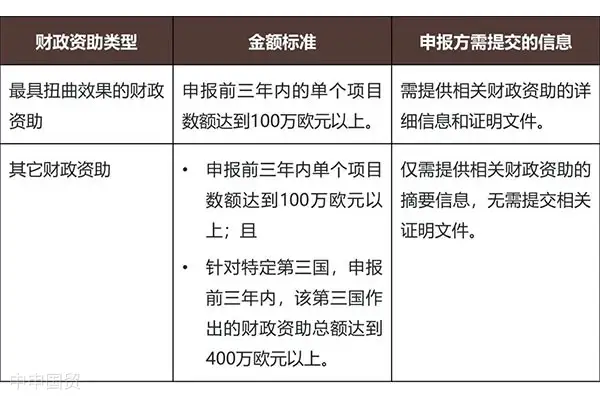

Information on foreign financial assistance: Depending on the type and amount of financial assistance, the filer needs to submit relevant information to the European Commission. At the same time, the information disclosure requirements for different types of financial assistance also vary.

Information on assessing the impact of foreign financial assistance on the EU market and possible positive impacts: including whether there is a bid in the concentrated transaction, the business and turnover of the target company and the filer, etc. The filer can also claim the possible positive impacts of the relevant financial assistance on the EU market.

II. Scope of Information Provision in the Public Procurement Filing Procedure

The filing of public procurement procedures mainly focuses on the financial assistance with the most distorting effects. When the total amount of financial assistance received by a bidder does not reach the corresponding filing threshold, it needs to submit a corresponding statement stating that it has not reached the filing threshold and prove it by disclosing the relevant financial assistance received.

III. Special Provisions: Transactions Involving Investment Funds

The Implementing Regulation further clarifies that transactions involving investment funds or enterprises controlled by investment funds, under certain conditions, do not need to file the foreign financial assistance obtained by other investment funds (or portfolio companies controlled by such investment funds) managed by the same investment company but with different investors.

IV. Provisions on Key Procedural Matters

Prior consultation with the European Commission: The European Commission encourages filers of merger and acquisition transactions and public procurement procedures to conduct prior consultations, especially in determining the scope of financial - assistance - related information to be provided, in order to reduce the amount of information that the filer needs to submit.

Exemption from the obligation to submit specific information: The Implementing Rules stipulate that the filer can submit a written application to request the European Commission to exempt it from the obligation to submit specific information. For example, if the filer can provide sufficient reasons to prove that the relevant information cannot be reasonably obtained or that the relevant information is not necessary for the case review, the European Commission may exempt the requirement to submit specific information.

V.Summary and Suggestions

Although the Implementation Rules have made some improvements in the declaration requirements compared with the Draft Implementation Rules (for Soliciting Opinions), reducing the burden on the declarant, enterprises still face many challenges and uncertainties in the actual declaration process. Suggestions for export enterprises:

Enterprises should comprehensively sort out the financial assistance they have received according to the specific requirements of the Subsidy Regulations and the Implementation Rules.

Enterprises can use the information disclosure standards specified in the Implementation Regulations for different types of financial assistance to screen the information to be reported, especially those financial assistance that may be determined to have a market - distorting effect.

In daily operations and when planning specific transactions, enterprises should try to avoid involving financial assistance that may be determined to have the most market - distorting effect. When obtaining important goods and services provided by the government or state - owned institutions, market - based procedures should be adopted as much as possible to meet market conditions.

If necessary, enterprises can use the prior consultation system to communicate with the European Commission on issues such as the declaration requirements for relevant transactions and the scope of information required for declaration. This will help reduce the declaration burden and increase the clarity of whether a transaction needs to be declared.

Overall, although there are some challenges, through careful planning and preparation, Chinese enterprises can still successfully invest and conduct economic activities in the EU market. At the same time, close attention should be paid to the implementation of the Implementation Rules by the European Commission, as well as possible interpretations and changes of relevant regulations.

? 2025. All Rights Reserved. 滬ICP備2023007705號-2  PSB Record: Shanghai No.31011502009912

PSB Record: Shanghai No.31011502009912